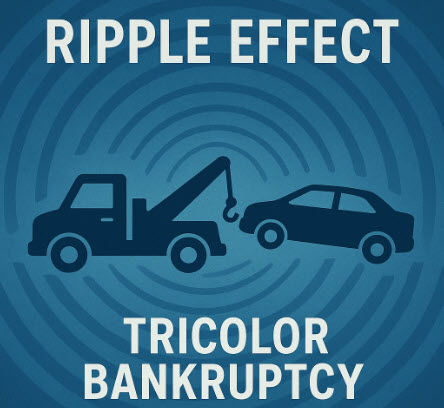

Most people don’t stop to think about what it really takes to run a repossession company. From the outside, it may look straightforward—an agent locates a vehicle, tows it away, and gets paid. Simple, right? Not quite. The reality is far more complex and far more expensive.

Repossession agents are typically only compensated when collateral is successfully recovered. If they spend hours running an account but can’t locate the vehicle, they walk away empty-handed.

Meanwhile, the bills keep coming: insurance premiums, licensing fees, payroll—and that’s just the tip of the iceberg. It’s not just the agents on the road who need to be paid—there are staff members dedicated to removing and inventorying personal property, scheduling customer pick-ups, and managing the flow of collateral through the lot. These are only a few of the many expenses that keep a repossession company running.

Space is another constant challenge.

Most repossession agents have limited storage capacity and depend on creditors to move vehicles quickly to auction. But with Tricolor’s bankruptcy, that flow comes to a screeching halt. Cars tied up in the process will sit in storage indefinitely, taking up valuable space and leaving fewer slots for new recoveries.

To make matters worse, agents fall into the category of unsecured creditors for any work performed before the bankruptcy filing. Translation: the chances of seeing payment for vehicles already repossessed range from slim to none.

Creditors play a crucial role

Creditors play a crucial role in minimizing the impact of the Tricolor bankruptcy on repossession agents.

By understanding the financial and operational strain on individual agents, prioritizing the quick movement of collateral, and maintaining clear communication, creditors can help ensure agents have the capacity and resources to continue repossessing effectively.

Small actions on the creditor’s side can make a big difference in keeping the process running smoothly for everyone involved.

Author: Bev Evancic

Bev.Evancic@ResourceManagement.com

Bev Evancic is a Senior Vice President at Resource Management Services, Inc. Prior to employment at RMS, Bev worked as the Collection and Recovery Manager at AT&T Universal Card, Citi, and Federated Department Stores. Bev started in the collection industry as a collector at an upscale clothing store in Cincinnati, Ohio. As a returned check and private label credit card collector, Bev gained a basic understanding of the collection industry that has not changed with the introduction of regulations. Her collection philosophy begins with the idea that businesses and customers benefit from preserving the customer relationship. First, collectors need to attempt to contact customers when it is convenient for the customer to discuss his/her financial condition and willingness/ability to pay. Second, you never collect money by intimidating or threatening customers. Third, businesses must make sure the debt is valid.

She has managed all phases of collection and recovery operations, including automated dialer units, bankruptcy, and legal units, skip tracing units, internal collections, outside collection agency networks, and Consumer Credit Counseling. As a Consultant for Resource Management Services, Inc., Bev has spearheaded collection and recovery best practices reviews for many top credit grantors. Her articles on dialer operations, agency management and bankruptcy best practices have been widely publicized.

She is well known and regarded as a specialty expert in the areas of: Repossession, Bankruptcy, Estate, Litigation, as well as Pre- and Post- Charge-off. Prior to joining Resource Management Services, Inc. in 1995, Bev managed the Recovery Department for AT&T Universal Card Services where she developed the bankruptcy, probate, internal and litigation processes.

She is the author of “Recovery Management: Collecting the Uncollectible Account.